First Time Buyer Buy-to-Let Mortgage

At Power Mortgages, we specialise in guiding first-time buyers through the Buy-to-Let mortgage process, ensuring you get the best deals and personalised advice to suit your investment goals.

Let us help you make your property investment journey smooth and successful.

Understanding First-Time Buyer Buy to Let Mortgages

First-time buyers often face unique challenges when entering the Buy-to-Let market. Unlike traditional residential mortgages, Buy-to-Let loans are designed specifically for property investors. A first-time buyer looking to purchase a rental property may find it more challenging to secure financing, as lenders often require additional criteria like rental income projections and a higher deposit.

Understanding how Buy-to-Let mortgages work and the factors that lenders consider can help you navigate the process with confidence. The main focus will be on your property’s rental potential, as lenders will want to ensure the rent will cover the mortgage payments.

It’s essential to be prepared with a clear plan for your rental property, including rental income expectations, as this will be a crucial part of your mortgage application. A mortgage broker can help explain the different types of Buy-to-Let loans available and guide you through the approval process.

Understanding First-Time Buyer Buy to Let Mortgages

First-time buyers often face unique challenges when entering the Buy-to-Let market. Unlike traditional residential mortgages, Buy-to-Let loans are designed specifically for property investors. A first-time buyer looking to purchase a rental property may find it more challenging to secure financing, as lenders often require additional criteria like rental income projections and a higher deposit.

Understanding how Buy-to-Let mortgages work and the factors that lenders consider can help you navigate the process with confidence. The main focus will be on your property’s rental potential, as lenders will want to ensure the rent will cover the mortgage payments.

It’s essential to be prepared with a clear plan for your rental property, including rental income expectations, as this will be a crucial part of your mortgage application. A mortgage broker can help explain the different types of Buy-to-Let loans available and guide you through the approval process.

Eligibility and Requirements for First-Time Buy-to-Let Buyers

When applying for a Buy-to-Let mortgage as a first-time buyer, there are specific eligibility requirements that must be met. Lenders typically want to see a minimum deposit of around 25% of the property's value. The larger your deposit, the better your chances of securing a competitive deal.

In addition to the deposit, your personal financial situation will be assessed. Lenders will take a close look at your credit score, income, and overall financial health to ensure you can handle the mortgage repayments.

As a first-time buyer, you should also be aware of other costs involved in purchasing a property, such as stamp duty, legal fees, and maintenance expenses. It’s essential to factor these into your budget to avoid any surprises along the way.

How a Mortgage Broker Can Help First-Time Buyers Secure Buy-to-Let Mortgages

A mortgage broker can be an invaluable resource for first-time Buy-to-Let investors, offering expert advice and support throughout the mortgage process. They have access to a wide range of lenders, including specialist lenders who cater to first-time buyers, and can help you compare mortgage deals to find the most competitive rates.

Mortgage brokers will help you navigate the complexities of the Buy-to-Let market by explaining the different mortgage options, such as fixed-rate or variable-rate loans, and helping you choose the best option for your financial situation.

Working with a specialist mortgage broker like Power Mortgages also ensures that you submit a complete and accurate application. They can help you prepare the necessary documents, gather income information, and ensure that everything is in order before submission, giving you the best chance of success.

How a Mortgage Broker Can Help First-Time Buyers Secure Buy to Let Mortgages

A mortgage broker can be an invaluable resource for first-time Buy-to-Let investors, offering expert advice and support throughout the mortgage process. They have access to a wide range of lenders, including specialist lenders who cater to first-time buyers, and can help you compare mortgage deals to find the most competitive rates.

Mortgage brokers will help you navigate the complexities of the Buy-to-Let market by explaining the different mortgage options, such as fixed-rate or variable-rate loans, and helping you choose the best option for your financial situation.

Working with a specialist mortgage broker like Power Mortgages also ensures that you submit a complete and accurate application. They can help you prepare the necessary documents, gather income information, and ensure that everything is in order before submission, giving you the best chance of success.

Frequently Asked Questions

Frequently Asked Questions about First Time Buyer Buy-to-Let Mortgages

What is a First-Time Buyer Buy-to-Let Mortgage?

A First-Time Buyer Buy-to-Let Mortgage allows first-time buyers to purchase a property to rent out. It’s a mortgage designed specifically for people who have never owned a rental property before.

Can I get a Buy-to-Let mortgage if I’m a first-time buyer?

Yes, first-time buyers can apply for a Buy-to-Let mortgage, but lenders typically require a larger deposit and assess your rental income potential to ensure the mortgage can be serviced through rent.

How much deposit do I need for a First-Time Buyer Buy-to-Let Mortgage?

The typical deposit required is around 25% of the property’s value, depending on the lender and your financial circumstances.

What do lenders look for when approving a First-Time Buyer Buy-to-Let Mortgage?

Lenders will primarily assess the rental income of the property, your credit score, your deposit, and your overall financial situation to ensure you can manage the mortgage payments.

How do I know if I will get approved for a First-Time Buyer Buy-to-Let Mortgage?

Lenders will look at factors such as your credit history, financial stability, and rental income potential. Working with a mortgage broker can help ensure you meet the necessary criteria and improve your chances of approval.

What is the minimum rental income required for a First-Time Buyer Buy-to-Let Mortgage?

Most lenders require the rental income to cover at least 125-145% of the mortgage payments. This ensures that the property generates enough income to cover the loan repayment.

Do I need a job to apply for a First-Time Buyer Buy-to-Let Mortgage?

While you don’t necessarily need a job, lenders will assess your income. If you’re employed, your salary will be considered, or if you have other sources of income, such as savings or investments, this will also be taken into account.

Can I apply for a Buy-to-Let mortgage without any previous landlord experience?

Yes, it is possible, but lenders may require you to demonstrate that you can manage the property, or they may require a larger deposit or higher rental yield.

Can I remortgage my property to release equity as a first-time buyer?

The process can take several weeks, depending on the complexity of your portfolio and the lender’s procedures.

Are there any fees associated with buy-to-let debt consolidation?

Additional costs may include stamp duty, legal fees, valuation fees, and ongoing maintenance costs for the property.

What types of Buy-to-Let mortgages are available for first-time buyers?

Common types of Buy-to-Let mortgages include fixed-rate, variable-rate, and tracker mortgages. Each type has its own pros and cons depending on the investor’s financial situation.

Can I get a Buy-to-Let mortgage if I’ve never owned property before?

Yes, first-time buyers can apply for Buy-to-Let mortgages, but eligibility requirements may differ from residential mortgages, and the process can be more complex.

For more detailed information, speak to one of our mortgage specialists to assess your specific situation.

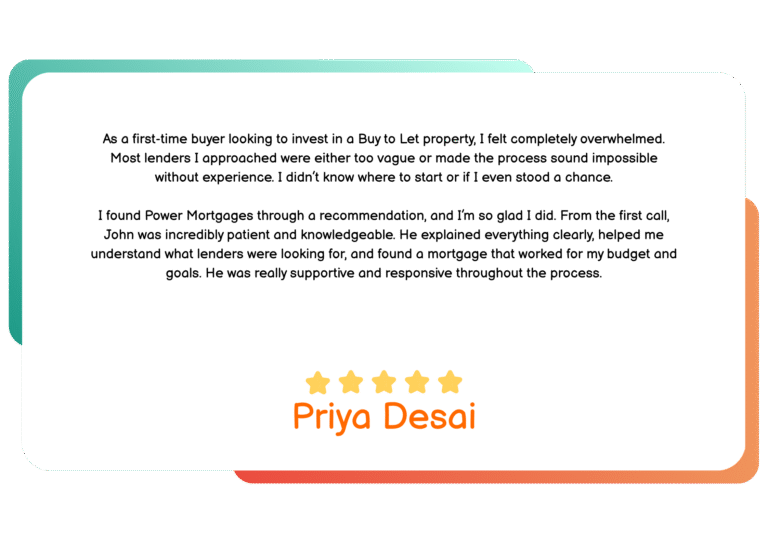

Client Testimonial

Client Testimonial

“As a first-time buyer looking to invest in a Buy to Let property, I felt completely overwhelmed. Most lenders I approached were either too vague or made the process sound impossible without experience. I didn’t know where to start or if I even stood a chance.

I found Power Mortgages through a recommendation, and I’m so glad I did. From the first call, John was incredibly patient and knowledgeable. He explained everything clearly, helped me understand what lenders were looking for, and found a mortgage that worked for my budget and goals. He was really supportive and responsive throughout the process.”

Priya Desai