Switch to a Buy-to-Let Mortgage

If you’re considering switching your current mortgage to a Buy to Let mortgage, it can be an excellent way to optimise your investment and maximise your rental income.

A specialist adviser can guide you through the process, helping you assess your options, compare lenders, and find the best rates based on your individual circumstances. They’ll ensure the switch is smooth and hassle-free, taking care of all the paperwork and helping you understand the potential benefits of switching.

Why Consider Switching to a Buy-to-Let Mortgage?

Switching to a Buy-to-Let mortgage can be a strategic decision if you own rental properties or are looking to enter the property investment market. With a Buy to Let mortgage, you can optimise your financial potential by leveraging your property's rental income.

This type of mortgage allows you to benefit from tax advantages, as mortgage interest payments are often tax-deductible. Additionally, switching could result in better rates or more favourable terms, potentially improving cash flow and overall profitability.

If you’re already an existing landlord, switching can help you reassess your loan to match the current property market or refinance for more competitive terms. A specialist mortgage broker can help you navigate these options efficiently.

Why Consider Switching to a Buy to Let Mortgage?

Switching to a Buy to Let mortgage can be a strategic decision if you own rental properties or are looking to enter the property investment market. With a Buy to Let mortgage, you can optimise your financial potential by leveraging your property’s rental income.

This type of mortgage allows you to benefit from tax advantages, as mortgage interest payments are often tax-deductible. Additionally, switching could result in better rates or more favourable terms, potentially improving cash flow and overall profitability.

If you’re already an existing landlord, switching can help you reassess your loan to match the current property market or refinance for more competitive terms. A specialist mortgage broker can help you navigate these options efficiently.

What You Need to Consider Before Switching

Before switching, it's important to evaluate your current situation. Are you achieving the rental income you expected? Do you need to adjust your monthly repayments? Switching can give you an opportunity to review your loan term and borrowing limits.

The property’s value, your rental yield, and the potential future market conditions should also be taken into account when making a decision. It’s worth discussing your future property goals with a professional to ensure the switch benefits you in the long term.

Having a clear understanding of fees and the implications of switching, such as early repayment charges or additional costs, is key. A mortgage adviser can provide clarity and explain these factors to avoid any surprises down the line.

How a Mortgage Broker Can Help

A specialist mortgage broker is essential in making the switch process seamless. They have access to a wide range of lenders and can compare deals to find the best mortgage rates suited to your needs.

They can guide you through the paperwork, help you assess the value of your property, and ensure all the eligibility criteria are met. They will also act as your advocate, liaising with lenders to make the process smoother and faster.

In addition, mortgage brokers can offer advice on structuring your mortgage in the most tax-efficient way, ensuring that your Buy to Let investment continues to be a profitable venture. Their expertise ensures you make informed decisions and secure the best possible deal.

How a Mortgage Broker Can Help

A specialist mortgage broker is essential in making the switch process seamless. They have access to a wide range of lenders and can compare deals to find the best mortgage rates suited to your needs.

They can guide you through the paperwork, help you assess the value of your property, and ensure all the eligibility criteria are met. They will also act as your advocate, liaising with lenders to make the process smoother and faster.

In addition, mortgage brokers can offer advice on structuring your mortgage in the most tax-efficient way, ensuring that your Buy to Let investment continues to be a profitable venture. Their expertise ensures you make informed decisions and secure the best possible deal.

Frequently Asked Questions

Frequently Asked Questions about Switch to a Buy-to-Let Mortgage

Can I rent out my home with a residential mortgage?

Generally, renting out your home on a residential mortgage without notifying your lender is not allowed. If you plan to rent out your property, you will need to inform your lender and potentially switch to a Buy to Let mortgage.

How do I switch to a Buy-to-Let mortgage?

To switch to a Buy to Let mortgage, you need to apply for a new mortgage product that suits your rental property. The process may involve changing from a residential mortgage, and a specialist mortgage adviser can help you navigate the switch.

Can I switch my residential mortgage to a Buy-to-Let mortgage?

Yes, you can switch from a residential mortgage to a Buy to Let mortgage if you’re planning to rent out your property. You’ll need to inform your lender, and they will assess your application for suitability.

What deposit is required for a Buy-to-Let mortgage?

Typically, Buy to Let mortgages require a deposit of at least 25% of the property’s value, but this can vary depending on the lender and your financial profile.

Can I get a Buy-to-Let mortgage if I have no prior landlord experience?

Yes, it is possible to get a Buy to Let mortgage as a first-time landlord. However, some lenders may require you to demonstrate experience or a suitable financial background. A specialist adviser can help you find the right lender.

How do lenders assess Buy-to-Let mortgage applications?

Lenders primarily assess Buy to Let mortgage applications based on the rental income the property can generate. They may also consider your financial situation and credit history, but the potential income from the property is a key factor.

Are Buy-to-Let mortgages interest-only or repayment?

Buy to Let mortgages can be either interest-only or repayment. An interest-only mortgage means you only pay the interest each month, with the loan principal due at the end of the term. Repayment mortgages include both principal and interest payments.

What are the benefits of switching to a Buy-to-Let mortgage?

Switching to a Buy to Let mortgage allows you to generate rental income, benefit from property value growth, and potentially save on taxes. It’s also a strategic move if you want to hold on to your property during market fluctuations.

How do I know if switching to a Buy-to-Let mortgage is the right option for me?

It’s important to consider your long-term goals and financial situation. If you’re planning to rent out your property and want to optimise your financial returns, switching to a Buy to Let mortgage could be a smart choice. A specialist adviser can help you assess your options.

What costs are involved in switching to a Buy-to-Let mortgage?

Costs may include arrangement fees, legal fees, valuation fees, and potential early repayment charges if you’re switching from an existing mortgage. A mortgage adviser can guide you on all potential costs and help you plan accordingly.

Can I switch to a Buy-to-Let mortgage if my property is already rented?

Yes, if your property is already rented, you may still be able to switch to a Buy to Let mortgage. However, lenders may have specific requirements regarding the rental agreement and the income generated by the property.

How can a mortgage adviser help with switching to a Buy-to-Let mortgage?

A specialist mortgage adviser can guide you through the entire process, from assessing your eligibility to finding the best mortgage deals. They can help ensure you get the most competitive rates, provide advice on managing your property portfolio, and support you in making the right choice for your situation

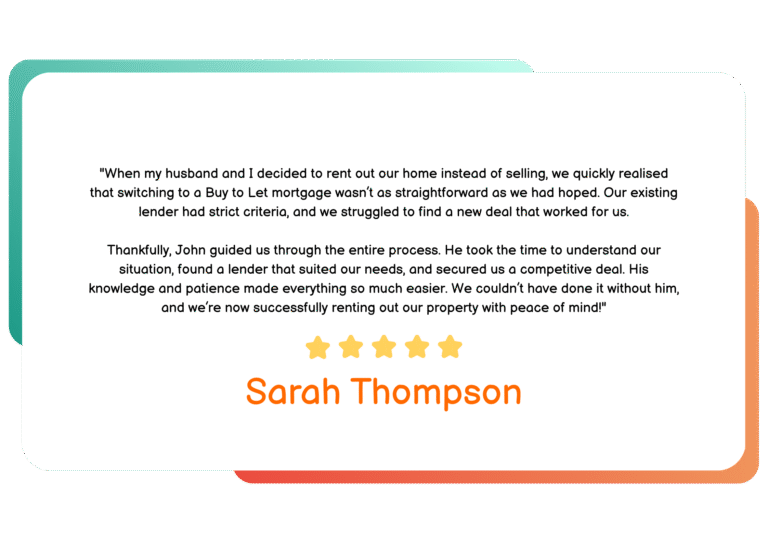

Client Testimonial

“Managing a growing portfolio of properties was starting to become a real headache — multiple renewal dates, scattered lender terms, and rising rates. I was losing time and money trying to juggle it all on my own.

Mandeep took the pressure off completely. He streamlined everything into a more manageable structure and found a deal that gave me far better flexibility. What I really appreciated was how he looked at the bigger picture, not just the immediate mortgage need. He genuinely cared about my long-term goals.”

Sarah Thompson

Client Testimonial