Buy-to-Let

Mortgage Ending

As your Buy to Let mortgage term comes to an end, it’s important to review your options to ensure you’re getting the best deal for your investment. Whether you’re looking to remortgage, switch lenders, or explore new opportunities, the right guidance can make all the difference.

A specialist adviser will help you navigate the remortgage process, identify the most competitive rates, and ensure you understand your options moving forward. They’ll assist with comparing deals, managing paperwork, and securing the best possible terms based on your financial goals and rental income.

What Happens When Your Buy-to-Let Mortgage Ends?

When your Buy-to-Let mortgage term ends, you’re typically moved onto the lender’s standard variable rate (SVR), which may be higher than what you’ve been paying. This can increase your monthly repayments, reducing your overall cash flow. It’s important to take action before your mortgage expires to avoid paying more than necessary.

If you’re still happy with your lender and their current rates, you can simply renew the mortgage or remortgage with the same provider. However, it’s often worth shopping around to see if you can secure a better deal. A remortgage could save you money and unlock more favourable terms.

Consulting with a specialist adviser can help you assess your situation and determine whether remortgaging or switching lenders is the best route for your property portfolio. They’ll consider your long-term financial goals and ensure you’re getting the most competitive rates available.

What Happens When Your Buy to Let Mortgage Ends?

When your Buy to Let mortgage term ends, you’re typically moved onto the lender’s standard variable rate (SVR), which may be higher than what you’ve been paying. This can increase your monthly repayments, reducing your overall cash flow. It’s important to take action before your mortgage expires to avoid paying more than necessary.

If you’re still happy with your lender and their current rates, you can simply renew the mortgage or remortgage with the same provider. However, it’s often worth shopping around to see if you can secure a better deal. A remortgage could save you money and unlock more favourable terms.

Consulting with a specialist adviser can help you assess your situation and determine whether remortgaging or switching lenders is the best route for your property portfolio. They’ll consider your long-term financial goals and ensure you’re getting the most competitive rates available.

Why You Should Consider Remortgaging Your Buy-to-Let Property

Remortgaging your Buy to Let property at the end of your mortgage term can provide you with several benefits. If property values have increased, it could also offer the opportunity to release additional equity for further investments or improvements. It’s a way of managing your property portfolio effectively, even as your financial situation changes.

Another reason to consider remortgaging is to secure a better interest rate. With the market constantly evolving, there may be more attractive deals available, which could reduce your monthly repayments. Over time, even a small reduction in interest can make a significant difference to your overall profits.

Working with a specialist adviser ensures you get access to exclusive deals that might not be available directly through lenders. They’ll compare the market for you, making the process much quicker and easier while helping you choose the most suitable product for your needs.

The Role of a Specialist Adviser in the Remortgaging Process

A specialist adviser plays a crucial role when it comes to remortgaging your Buy to Let property. Their in-depth knowledge of the market means they can guide you through the entire process, from comparing mortgage products to helping you complete the necessary paperwork.

They’ll evaluate your existing loan and property portfolio, ensuring that the terms you secure are in line with your financial objectives. They will also identify opportunities to unlock additional funds or adjust your repayment structure to better suit your cash flow needs.

By using their expertise, you’ll avoid the stress of navigating the remortgaging process alone and ensure that you’re making informed decisions that align with your investment goals.

The Role of a Specialist Adviser in the Remortgaging Process

A specialist adviser plays a crucial role when it comes to remortgaging your Buy to Let property. Their in-depth knowledge of the market means they can guide you through the entire process, from comparing mortgage products to helping you complete the necessary paperwork.

They’ll evaluate your existing loan and property portfolio, ensuring that the terms you secure are in line with your financial objectives. They will also identify opportunities to unlock additional funds or adjust your repayment structure to better suit your cash flow needs.

By using their expertise, you’ll avoid the stress of navigating the remortgaging process alone and ensure that you’re making informed decisions that align with your investment goals.

Frequently Asked Questions

Frequently Asked Questions about

Buy-to-Let Mortgage Ending

What happens when my Buy-to-Let mortgage term ends?

When your Buy to Let mortgage term ends, you’ll need to either repay the outstanding loan balance or arrange a remortgage to secure new terms. If you don’t make a payment or find a new deal, you could face legal action from the lender.

Can I switch to a new Buy-to-Let mortgage after my current term ends?

Yes, you can remortgage your Buy to Let property to secure a new deal after your current term ends. A specialist adviser can help you find the best rates and terms available.

What are my options if I can’t repay my Buy-to-Let mortgage in full?

If you can’t repay the mortgage in full, you may need to discuss your options with your lender, such as remortgaging or selling the property. A mortgage adviser can assist you in finding the best course of action

Will my mortgage lender allow me to switch to a standard residential mortgage at the end of my Buy-to-Let term?

It’s possible to switch to a standard residential mortgage, but this depends on your lender’s policies. You may need to sell the property or meet certain conditions to make the switch.

Do I have to pay penalties when my Buy-to-Let mortgage ends?

Some Buy to Let mortgages have early repayment charges if you end the term early or switch to a new mortgage. However, this will depend on your lender and the terms of your current mortgage agreement.

Can I remortgage my Buy-to-Let property when the mortgage term ends?

Yes, you can remortgage your Buy to Let property when your mortgage term ends. This could allow you to get a better rate, increase your loan amount, or switch to an interest-only option.

Should I consider selling my Buy-to-Let property when the mortgage ends?

If your mortgage payments are becoming unmanageable or if property prices have risen significantly, selling could be a good option. A specialist adviser can help you weigh up the pros and cons.

What happens if my Buy-to-Let mortgage is in arrears when the term ends?

If your mortgage is in arrears, you’ll need to make arrangements with your lender to clear the outstanding balance. You may be able to remortgage or sell the property to clear the debt.

Can I extend the term of my Buy-to-Let mortgage after it ends?

In some cases, you may be able to extend the term of your Buy to Let mortgage. This will depend on your lender’s policies, your age, and the financial viability of the property.

Can I still apply for a Buy-to-Let mortgage if I’m over 70 when the term ends?

It may be more difficult to get a Buy to Let mortgage if you’re over 70, but some lenders offer mortgages for older borrowers. A mortgage adviser can help find lenders with more flexible terms.

What documents will I need when my Buy-to-Let mortgage ends?

You may need to provide updated financial statements, rental income details, and proof of property value when seeking a remortgage or new terms for your Buy to Let property.

How can a specialist adviser help me when my Buy-to-Let mortgage ends?

A specialist adviser can help you navigate your options when your Buy to Let mortgage ends, from remortgaging and securing better rates to advising on selling or repaying the loan.

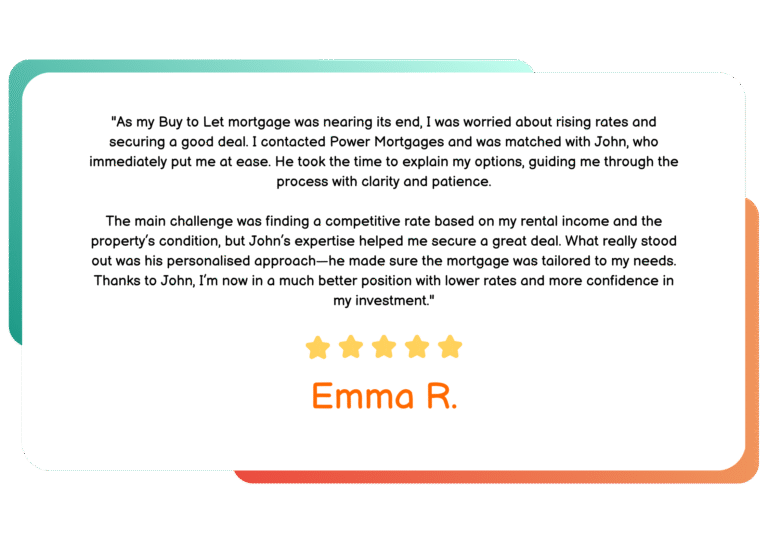

Client Testimonial

“As my Buy to Let mortgage was nearing its end, I was worried about rising rates and securing a good deal. I contacted Power Mortgages and was matched with John, who immediately put me at ease. He took the time to explain my options, guiding me through the process with clarity and patience.

The main challenge was finding a competitive rate based on my rental income and the property’s condition, but John’s expertise helped me secure a great deal. What really stood out was his personalised approach—he made sure the mortgage was tailored to my needs. Thanks to John, I’m now in a much better position with lower rates and more confidence in my investment.”

Emma R.

Client Testimonial