HMO Refurbishment Mortgage

Refurbishing an HMO property is a smart way to boost rental income and enhance tenant appeal, but securing the right mortgage for these improvements can be challenging.

A specialist adviser can simplify the process by assessing your goals, finding lenders offering suitable HMO refurbishment products, and guiding you through the application to ensure a seamless experience.

Understanding HMO Refurbishment Mortgages

HMO refurbishment mortgages are tailored to help landlords finance upgrades and improvements to Houses in Multiple Occupation (HMO). These mortgages allow you to invest in renovations that can increase rental income and property value.

Lenders offering HMO refurbishment mortgages often have specific criteria, such as requiring a minimum property value or rental yield. Understanding these requirements is essential for a successful application.

It’s important to note that the loan amount is usually linked to the projected rental income post-refurbishment. This means planning your upgrades carefully to meet lender expectations and maximise your borrowing potential.

Understanding HMO Refurbishment Mortgages

HMO refurbishment mortgages are tailored to help landlords finance upgrades and improvements to Houses in Multiple Occupation (HMO). These mortgages allow you to invest in renovations that can increase rental income and property value.

Lenders offering HMO refurbishment mortgages often have specific criteria, such as requiring a minimum property value or rental yield. Understanding these requirements is essential for a successful application.

It’s important to note that the loan amount is usually linked to the projected rental income post-refurbishment. This means planning your upgrades carefully to meet lender expectations and maximise your borrowing potential.

Eligibility for HMO Refurbishment Mortgages

To qualify for an HMO refurbishment mortgage, you must typically demonstrate experience as a landlord or provide evidence of a solid property management plan. First-time HMO landlords may face more stringent criteria.

Lenders will assess the current state of your property and your plans for refurbishment, including cost estimates and expected rental yield. This helps them determine the viability of the project and the loan amount they can offer.

Your financial profile also plays a key role. Strong credit history, stable income, and sufficient deposit or equity in the property can significantly improve your chances of approval.

How a Specialist Adviser Can Help

Navigating the complexities of HMO refurbishment mortgages can be daunting, but a specialist adviser can make the process smoother. They have access to a wide network of lenders, including those who specialise in HMO loans.

An adviser can help tailor your application to meet lender criteria, ensuring your refurbishment plans align with borrowing requirements. This reduces the risk of delays or rejections.

Additionally, they provide invaluable support by negotiating competitive rates, guiding you through paperwork, and managing communication with lenders to streamline the entire process.

How a Specialist Adviser Can Help

Navigating the complexities of HMO refurbishment mortgages can be daunting, but a specialist adviser can make the process smoother. They have access to a wide network of lenders, including those who specialise in HMO loans.

An adviser can help tailor your application to meet lender criteria, ensuring your refurbishment plans align with borrowing requirements. This reduces the risk of delays or rejections.

Additionally, they provide invaluable support by negotiating competitive rates, guiding you through paperwork, and managing communication with lenders to streamline the entire process.

Frequently Asked Questions

Frequently Asked Questions about HMO Refurbishment Mortgages

What is an HMO refurbishment mortgage?

An HMO refurbishment mortgage is a specialist loan designed to finance renovations or improvements to Houses in Multiple Occupation (HMOs), helping landlords increase property value and rental income.

Can I get an HMO refurbishment mortgage as a first-time landlord?

Some lenders may require prior landlord experience, but there are options available for first-time landlords. A specialist adviser can help you find suitable lenders.

What types of renovations can an HMO refurbishment mortgage cover?

These mortgages can cover repairs, extensions, room conversions, or any work required to meet HMO licensing standards and increase rental yield.

How much can I borrow with an HMO refurbishment mortgage?

The amount you can borrow depends on the property’s current value, the projected post-renovation value, and anticipated rental income.

Do lenders consider the post-renovation value of the property?

Yes, many lenders assess the property’s post-renovation value when determining loan amounts, which can allow for larger borrowing.

What deposit is required for an HMO refurbishment mortgage?

Deposit requirements typically range from 20% to 40% of the current property value, though this can vary depending on the lender and your financial profile.

How do I prove the refurbishment work is completed?

Lenders usually require evidence such as invoices, completion certificates, or inspections to confirm that the agreed refurbishment has been carried out.

Can I remortgage an HMO after refurbishment?

Yes, after completing the renovations, you can remortgage based on the new property value, potentially unlocking additional funds or reducing your interest rate.

Are there additional fees with an HMO refurbishment mortgage?

Fees may include arrangement fees, valuation costs, and legal fees. A mortgage adviser can help you understand and plan for these costs.

Do I need an HMO licence before applying for a refurbishment mortgage?

It depends on the local council and the property’s size and use. A mortgage adviser can guide you through licensing requirements for your area.

How long does it take to get an HMO refurbishment mortgage?

The process can take several weeks, depending on the lender, the complexity of your application, and the scope of the planned renovations.

How can a specialist adviser help with an HMO refurbishment mortgage?

A specialist adviser can identify lenders, structure your application to highlight the property’s potential, and streamline the process to save you time and effort.

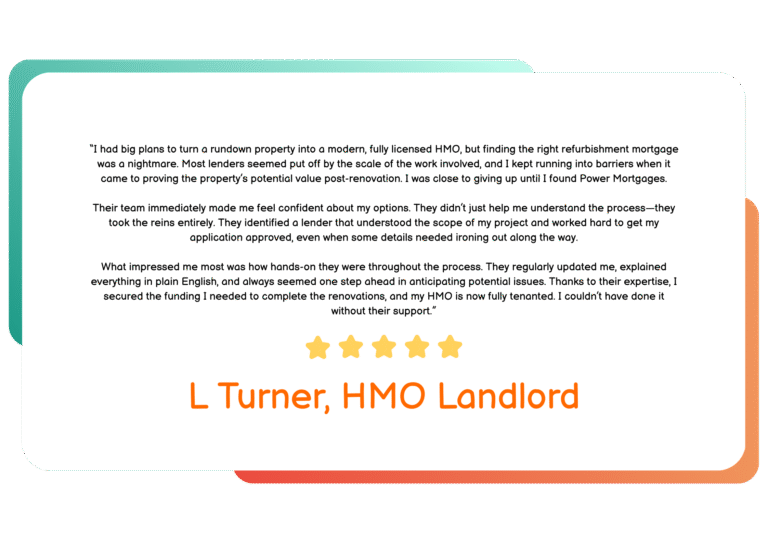

Client Testimonial

Client Testimonial

“I had big plans to turn a rundown property into a modern, fully licensed HMO, but finding the right refurbishment mortgage was a nightmare. Most lenders seemed put off by the scale of the work involved, and I kept running into barriers when it came to proving the property’s potential value post-renovation. I was close to giving up until I found Power Mortgages.

Their team immediately made me feel confident about my options. They didn’t just help me understand the process—they took the reins entirely. They identified a lender that understood the scope of my project and worked hard to get my application approved, even when some details needed ironing out along the way.

What impressed me most was how hands-on they were throughout the process. They regularly updated me, explained everything in plain English, and always seemed one step ahead in anticipating potential issues. Thanks to their expertise, I secured the funding I needed to complete the renovations, and my HMO is now fully tenanted. I couldn’t have done it without their support.”

L Turner, HMO Landlord